Woodborough’s Heritage

An ancient Sherwood Forest village, recorded in Domesday

Land Tax Act of 1692

The Land Tax was a land value tax levied in England from 1692 to 1963, though such taxes predate the best-known 1692 Act. Taxes on land date back to the Norman Conquest and beyond, and the Land Tax introduced in 1689 was a natural successor to taxation acts in 1671 and 1689, but the 1692 act "has been regarded as a turning point in the history of English revenue collection. It was from this Act that contemporaries and historians alike date what has come to be known as the eighteenth century Land Tax". The land tax elements of the 1671, 1689 and 1692 Acts were limited to one year but the 1798 Act made the tax perpetual (until it was abolished in 1963).

A Land Tax had also applied in Scotland from 1667. After the Acts of Union 1707, the Scottish charge was included in subsequent Acts of the Parliament of Great Britain.

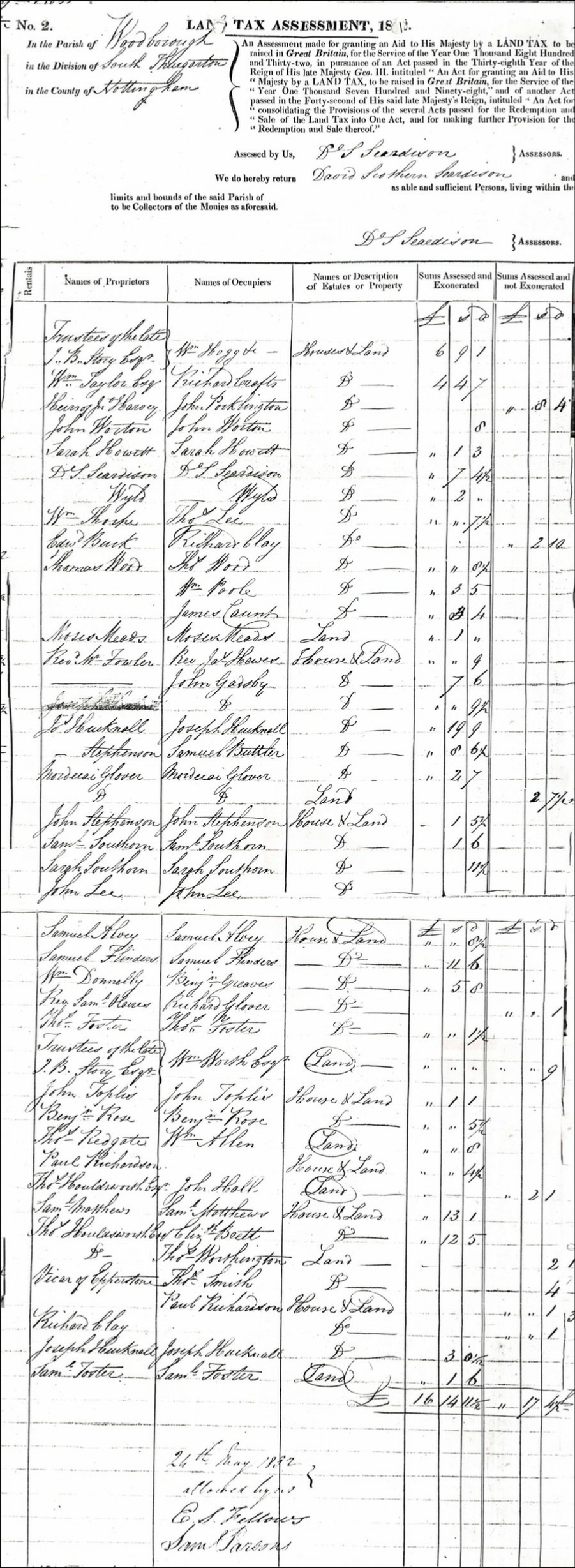

Below a typical completed Woodborough Land Tax Assessment form dated 24th May 1832

Land tax, like tithes, is another surviving charge placed upon land of which modern farmers bitterly complain. In its present form it was first levied in 1692 on real estates, offices and personnel property, including shops, carriages, wagons and servants. It was later confined entirely to land and so varied an assessment proved too difficult to maintain.

Throughout the 18th century the rate of tax fluctuated between one shilling and four shillings in the pound based upon the annual value, but not acreage, of the land, but in 1798 was fixed ‘perpetually’ at a rate of four shillings in the pound. Provision was made for landowners to redeem the annual tax with a lump sum which ‘exonerated’ them from further payments.

Land tax assessments assumed a further political importance in 1779 when they were used as the record of qualification to vote in Parliamentary elections and continued to be so until the Reform Act of 1832 provided for a separate register of electors.

Returns of the total valuation of a parish’s lands were made by local assessors who were nominated by special Commissioners appointed for the purpose (usually Justices of the Peace). A copy of the assessment was displayed on the Church door, to give an opportunity for appeal, and the amended assessment was sent to the Clerk of the Peace who enrolled it for electoral purposes.

Each parish was assessed to produce a certain total quota of tax, the rate which would provide the quota from the village’s assessment was fixed by the local assessors. Thus a parish’s quota tended to remain fixed, in spite of considerable changes in real value over periods of years.

The workings of 1798 was amended by Lloyd George in his 1909 Budget and down to 1949 each parish produced a quota of land tax by means of a rate which was not to be less than one penny and not to exceed one shilling in the pound.

Land Tax was not levied on agricultural land alone but could be demanded from owners of houses which had been built on land previously assessed.

The Finance Act of 1949 stabilises the rates of valuations on the basis of those paid for 1948/9 with a further provision that all Land Tax must henceforth be compulsorily redeemed at the death of the owner or a transfer of the land by sale, (so it will eventually as a tax disappear).

Acknowledgements:

- Wikipedia.

- Peter Saunders.

__________________________________________________________________________________________

| Navigate this site |

| 001 Timeline |

| 100 - 114 St Swithuns Church - Index |

| 115 - 121 Churchyard & Cemetery - Index |

| 122 - 128 Methodist Church - Index |

| 129 - 131 Baptist Chapel - Index |

| 132 - 132.4 Institute - Index |

| 129 - A History of the Chapel |

| 130 - Baptist Chapel School (Lilly's School) |

| 131 - Baptist Chapel internment |

| 132 - The Institute from 1826 |

| 132.1 Institute Minutes |

| 132.2 Iinstitute Deeds 1895 |

| 132.3 Institute Deeds 1950 |

| 132.4 Institute letters and bills |

| 134 - 138 Woodborough Hall - Index |

| 139 - 142 The Manor House Index |

| 143 - Nether Hall |

| 139 - Middle Manor from 1066 |

| 140 - The Wood Family |

| 141 - Manor Farm & Stables |

| 142 - Robert Howett & Mundens Hall |

| 200 - Buckland by Peter Saunders |

| 201 - Buckland - Introduction & Obituary |

| 202 - Buckland Title & Preface |

| 203 - Buckland Chapter List & Summaries of Content |

| 224 - 19th Century Woodborough |

| 225 - Community Study 1967 |

| 226 - Community Study 1974 |

| 227 - Community Study 1990 |

| 400 - 402 Drains & Dykes - Index |

| 403 - 412 Flooding - Index |

| 413 - 420 Woodlands - Index |

| 421 - 437 Enclosure 1795 - Index |

| 440 - 451 Land Misc - Index |

| 400 - Introduction |

| 401 - Woodborough Dykes at Enclosure 1795 |

| 402 - A Study of Land Drainage & Farming Practices |

| People A to H 600+ |

| People L to W 629 |

| 640 - Sundry deaths |

| 650 - Bish Family |

| 651 - Ward Family |

| 652 - Alveys of Woodborough |

| 653 - Alvey marriages |

| 654 - Alvey Burials |

| 800 - Footpaths Introduction |

| 801 - Lapwing Trail |

| 802 - WI Trail |